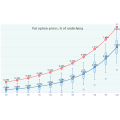

There are various pieces of evidence exist confirming that put options on wide equity indices are permanently overpriced by the market. The excess demand for the long portfolio protection is believed to be the main reason for this.

This research conducted using the OptionSmile platform underpins that observation and confirms that a put options selling has abnormally high expected profit.

However, on the risk-adjusted basis, such a short put strategy does not look so attractive due to the high volatility of results and regular huge drawdowns: the Sharpe ratio of a put selling, even with limited risk (spread strategy), is not so attractive and does not differ significantly from the Sharpe ratio of the outright long position in the underlying security.

Therefore, that high profitability of puts should be considered as a volatility premium rather than a market inefficiency.